Households in the US makes more money, why do so many people think otherwise?

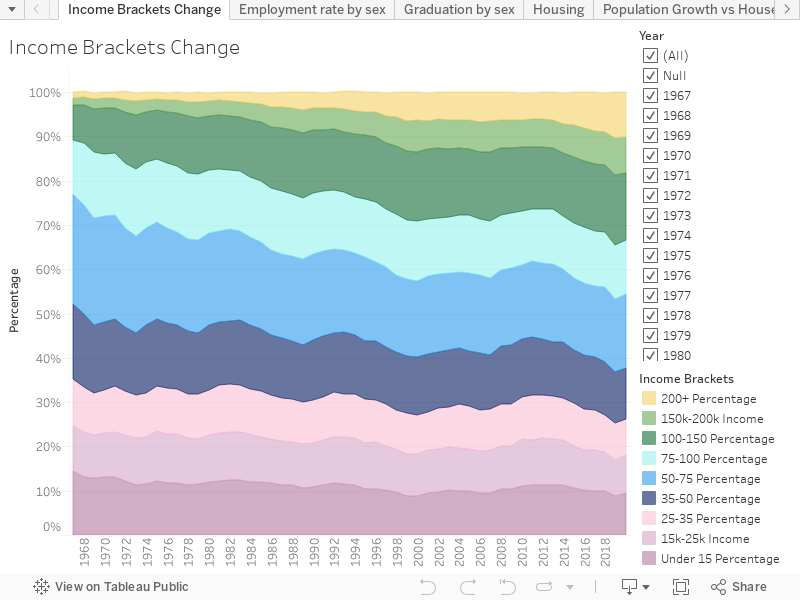

While scrolling Twitter, I stumbled upon Elon Musk's reply to Jeremy Horpedahl's tweet. He posted an area graph of change in household income brackets from 1970 to 2020 with the main takeaway "The number of rich households (> $150K) has exploded from 1.8 to 23.8 million. Very poor households (< $25K) shrunk from 24.7% to 18.1% (number rose slightly)". That, on the surface, contradicts the mainstream idea of "Rich getting richer and poor getting poorer" which probably explains Elon Musk's reply tweet, "Interesting...". The graph got me thinking about whether the economy is indeed working well for Americans or if there is, perhaps, a different explanation for this data. And finally, why do many people feel like we have a lower standard of life compared to 50 years ago.

First, I downloaded data provided by census.gov and double-checked the results myself. Indeed it looks as good as it seemed at first. Let's examine the data itself.

Indeed it looks as good as it seemed at first. We can see that a significant proportion of households have moved to higher income brackets. However, we can't just attribute it to a healthy economy and call it a day. First, we need to explore all possible factors that influence our findings.

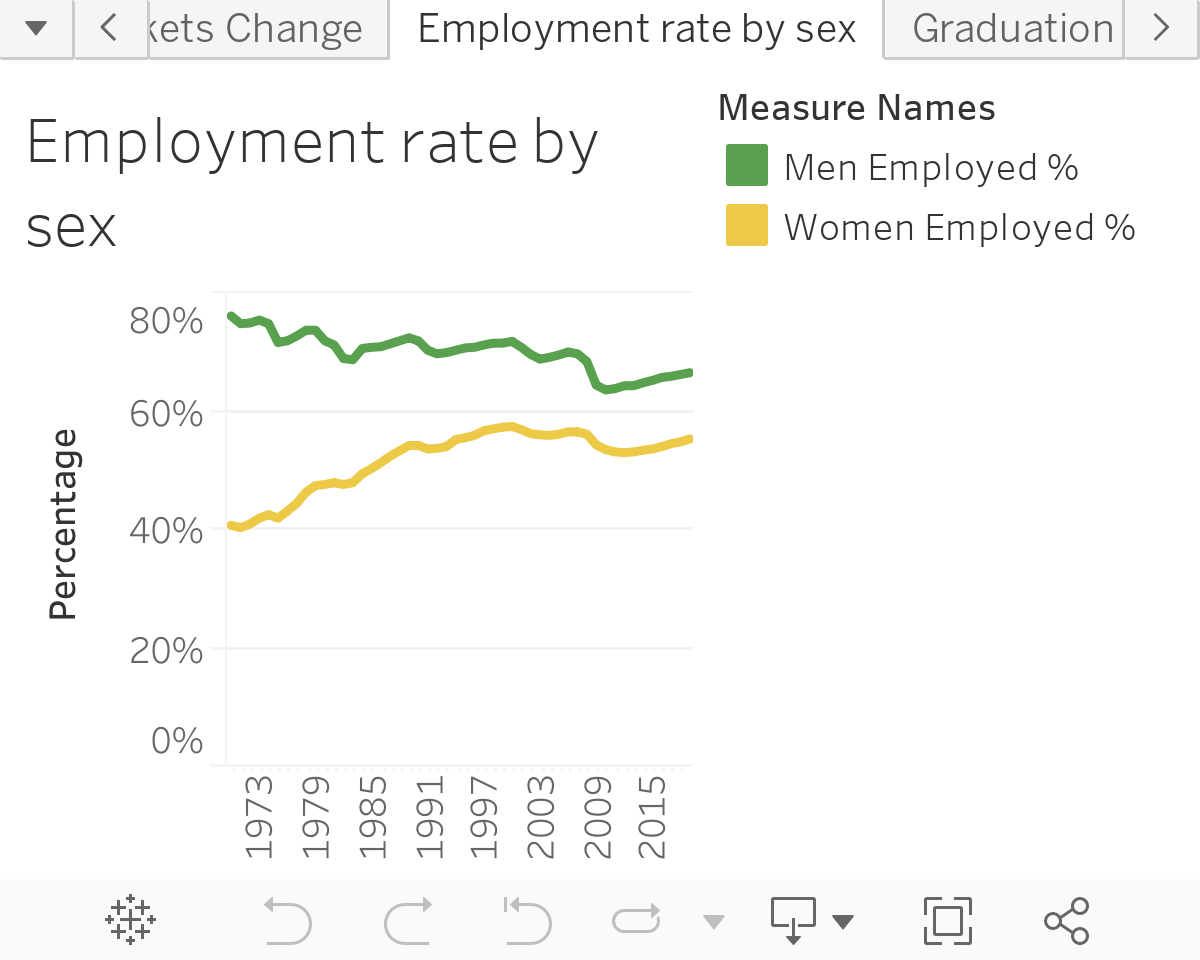

By definition, household income is a measure of the combined incomes of all people sharing a particular household or place of residence. Thus, my first assumption was that increasing women's participation in the labor force could significantly impact household income growth. Let's use Census data and look at how labor participation changed for both genders from 1970 to 2020. To achieve relevant and accurate results, we need to look at employment percentage from a labor force, not a share of a total population:

We can see the percentage of employed females has been increasing since 1970, peaked in 2000 and stabilized around 55,4%, which is a 15% increase over 1970. At the same time, male employment has fallen from 76.2% to 66.6%. Thus, more females entered the employed workforce than men who left it. Given the 2020 ratio of male-to-female at 49% to 51%, we may conclude that over the last 50 years, 2.3% of the labor population joined the labor force. However, we can't conclude that this change led to increased household income without studying households themselves. Moreover, when we look at the period from 1984 to 1989 when both females and males had a significant increase in employment, we see no to little increases in household income brackets. That may be caused by the fact that the more people get employed, especially among the younger population - the more new households are being created.

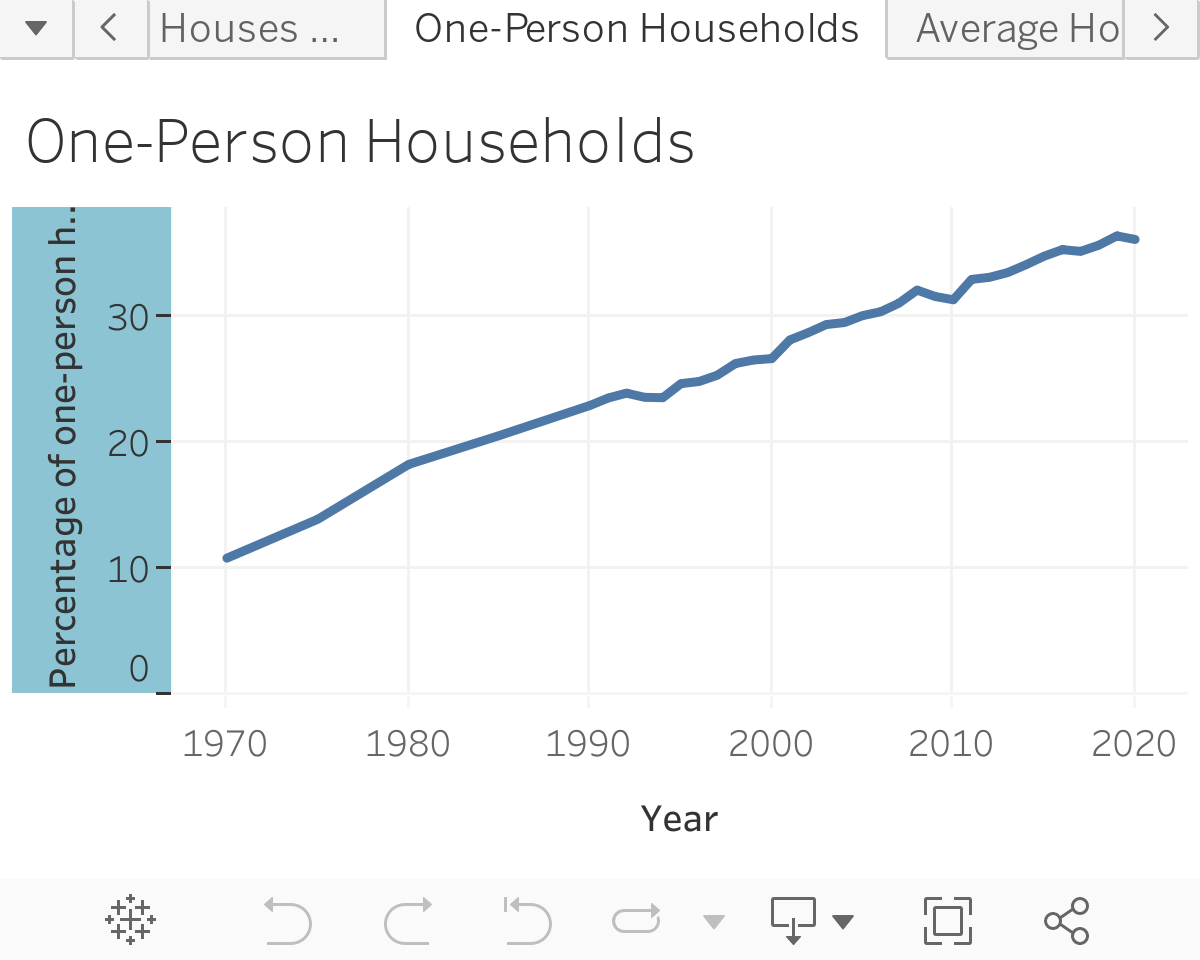

Given how household income is calculated, we can conclude that a household with two or more people is more likely to have a higher income than a single-person household. Thus, the increase in single-person households should negatively affect the household's income brackets growth and vice versa.

However, when we look at the graph of the percentage of the single-person households, we can see that it increased from 10.85% in 1970 to a staggering 36.20% in 2020. As a result, we can see the rate of single-person households tripled. However, the household's income only grew.

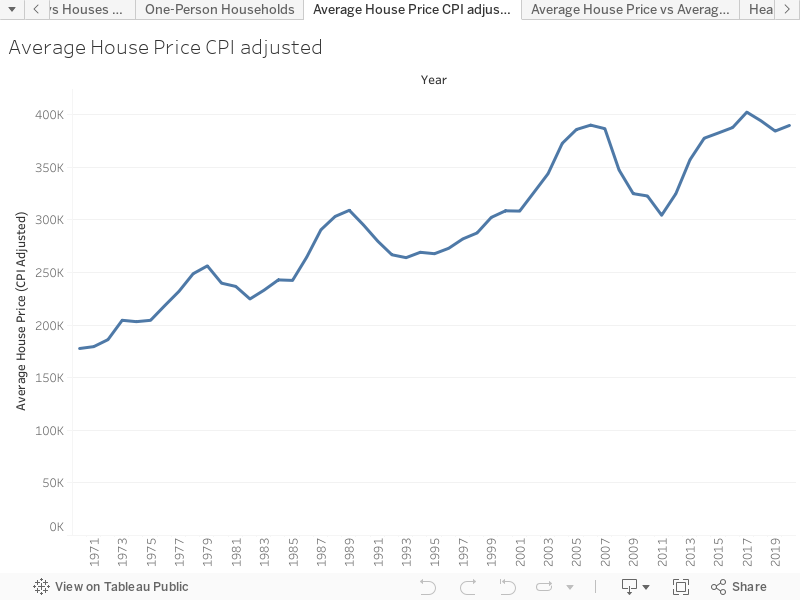

So far, all evidence seems to suggest that economic growth is present, and on a large scale, people indeed have a larger income than 50 years ago, as Mr. Horpedahl suggested. However, now we have to answer a much more complicated question - why does a large portion of the population feel like economically we lived better in 1970? According to Pew Research Center, 41% of polled people think that "Life in our country is worse than it was 50 years ago for people like me" against 37% who think otherwise. To understand why 41% of Americans feel that way, despite objective economic growth, we need to look at essential expenditures and the cost of living. Let's examine how housing prices changed over time. Federal Reserve has the data on average prices that were sold from 1970 to 2020. This time, in addition to cleaning up the data, we also have to make CPI adjustments to the price. Now let's look at the following graph:

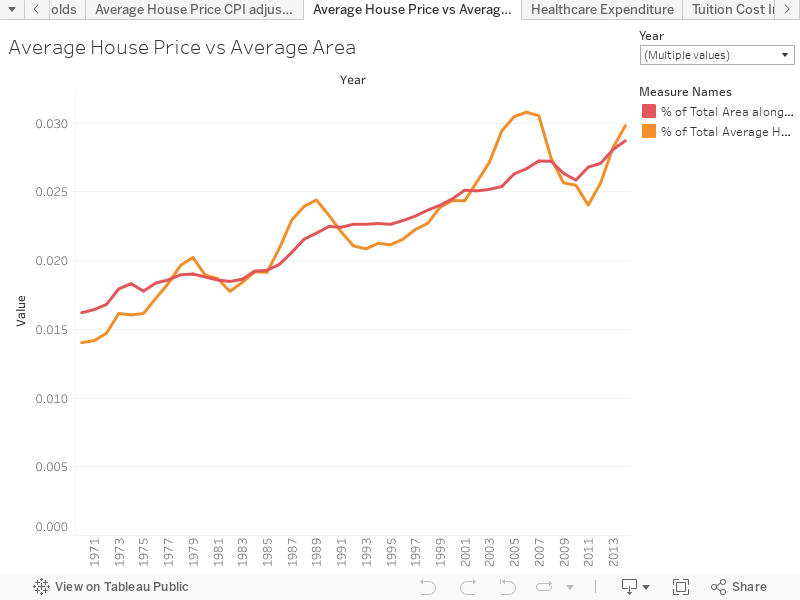

We can see that the average price for a house from 1970 to 2014 has risen by 2.12 times. That definitely could influence the way people feel about their economic opportunities. However, let's also try to find an answer to why housing prices have risen so significantly. We could compare the historical difference in the cost of raw materials such as steel, concrete, wood, stone, and brick/masonry, but it deserves a separate in-depth analysis. I suggest we focus on the other very important factor - square footage. Let's plot two graphs of average housing price and average housing area.

We can see that both graphs share similar local gains and losses, but what's most importantly, they both are constantly growing at a similar pace. Thus, the average house square footage in 2014 is 1.77 times higher than in 1970. There is no doubt that square footage is a prime parameter in determining housing price, given that zip code is not applicable in our case. Thus, the majority of the housing price increase can be explained by the growth of population appetite. Construction companies don't build the houses they want. They build houses that they can sell. Thus, the population is driving demand for larger homes logically leads to a higher cost of the latter. Similar conversations can be found about cars and how more affordable they were back in time. However, the same people want their cars to have all of the modern safety suits, more powerful and, at the same time, more efficient engines, more sophisticated technology inside, precise handling, and comfortable ride. That comes at a cost not just of R&D but also raw materials and a much more complicated build process.

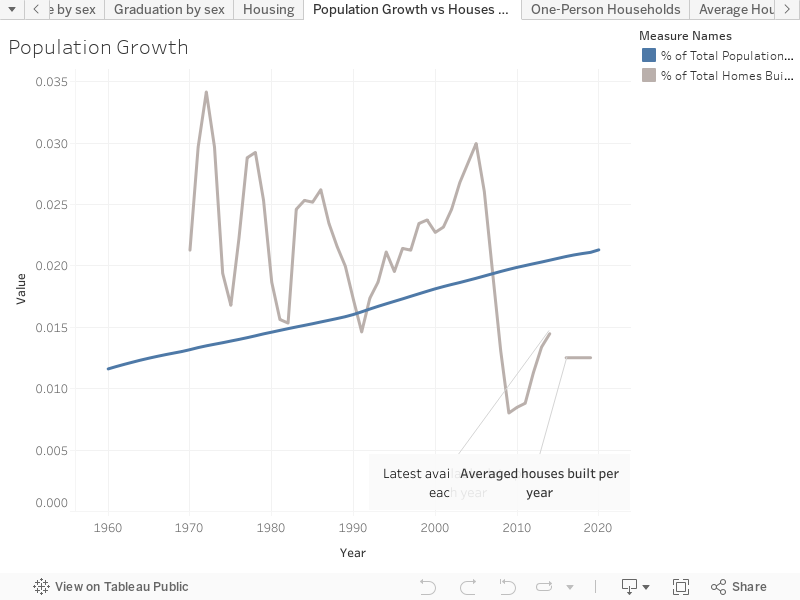

The other major factor in housing costs is the classical demand/supply ratio. Let's plot population grows over houses built:

We can see that since the economic crisis of 2008, construction of new houses has fallen to historically low numbers, and it hasn't made a full recovery yet. The data per year that I found ends in 2014. However, according to US Census data, only 3.46m houses were built between 2016 and 2019, on average, 865,000 units annually. We have a situation where the supply rate is decreasing while demand is steadily growing. Moreover, the land is a limited supply, and with constantly increasing demand, the price per square foot will keep increasing.

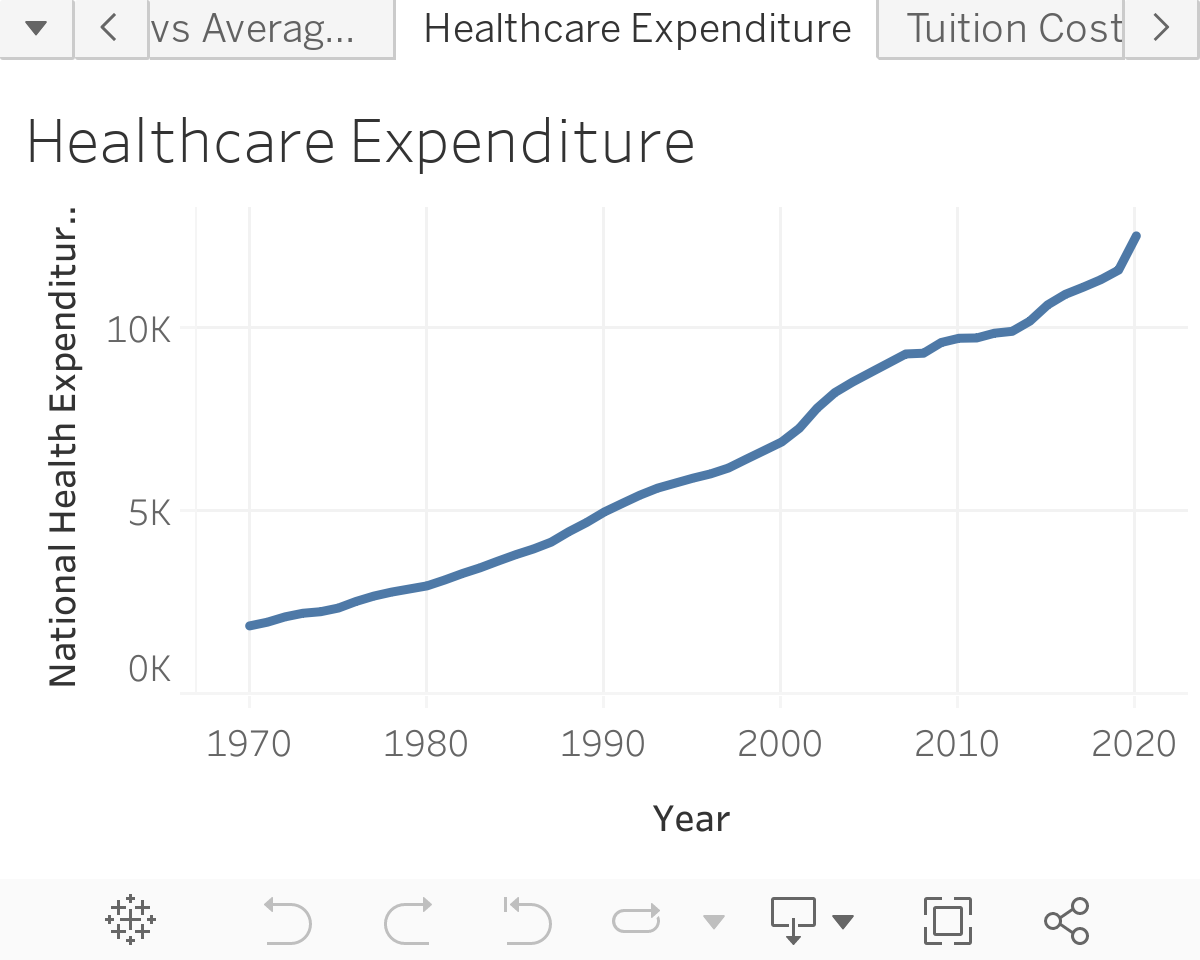

The other essential expenditure of every American is healthcare. Unfortunately, I couldn't find any historical data on the average cost of health insurance premiums. Therefore, we will have to use NHE data on total national health expenditures per capita from 1970 to 2020. Like with housing prices, we have to make CPI adjustments to expenditures. Let's plot the graph of Healthcare expenditure per capita (CPI adjusted) and analyze it.

We can see a staggering growth in healthcare expenditures from 1970 to 2020. Let's set the limit at 2019 as it hasn't been influenced by Covid19 yet. We can see that expenditure rose by more than 6 times. This significant cost difference impacts the economic well-being of bottom 50 percentile families to a higher degree than top 50 percentile families.

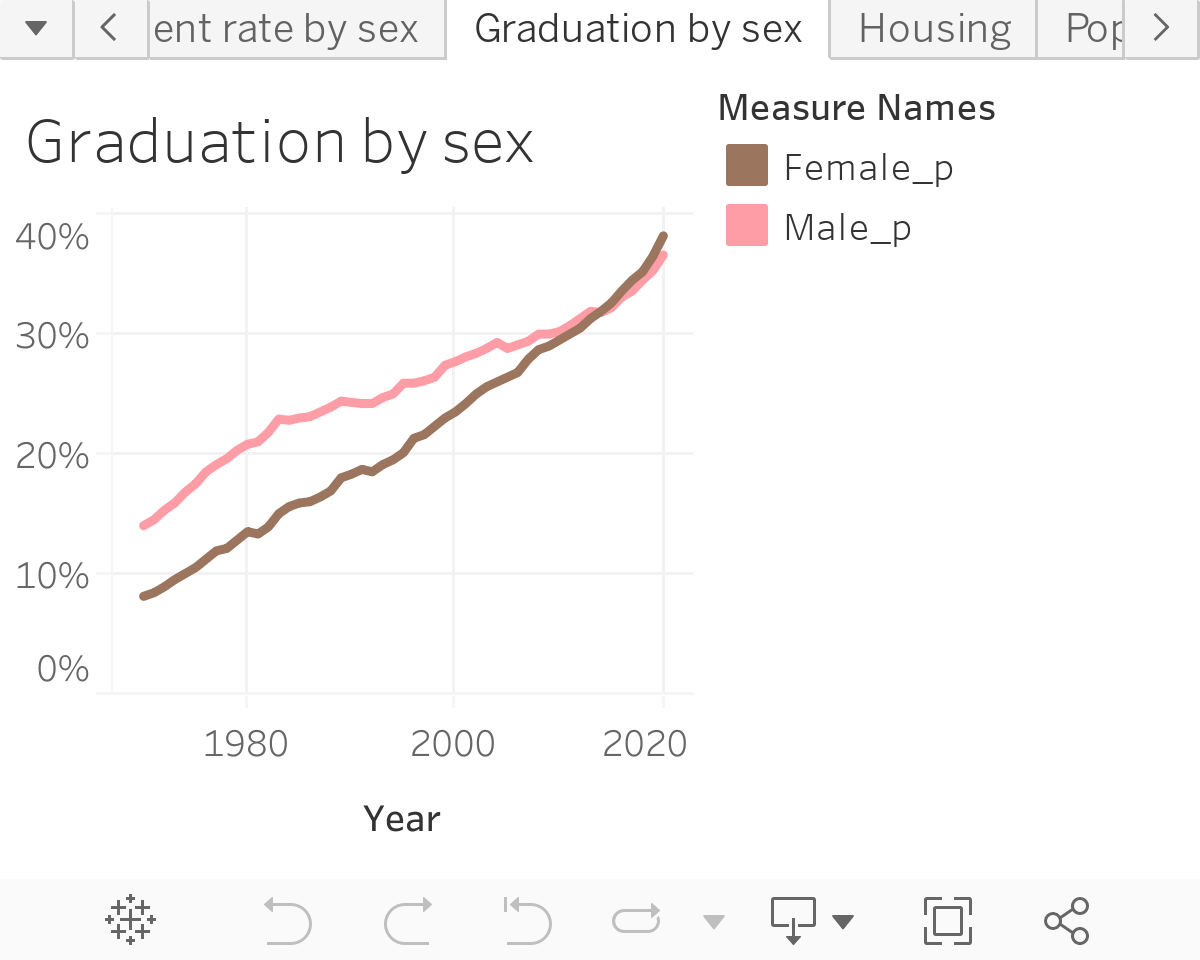

From the original graph, we can see that the income brackets that received the highest gains are those households that are making $150,000 and more. In 1970 those households only represented 3% of total households compared to 18.3% in 2020. Let's look at the percentage of graduates to see if we can spot any valuable insights:

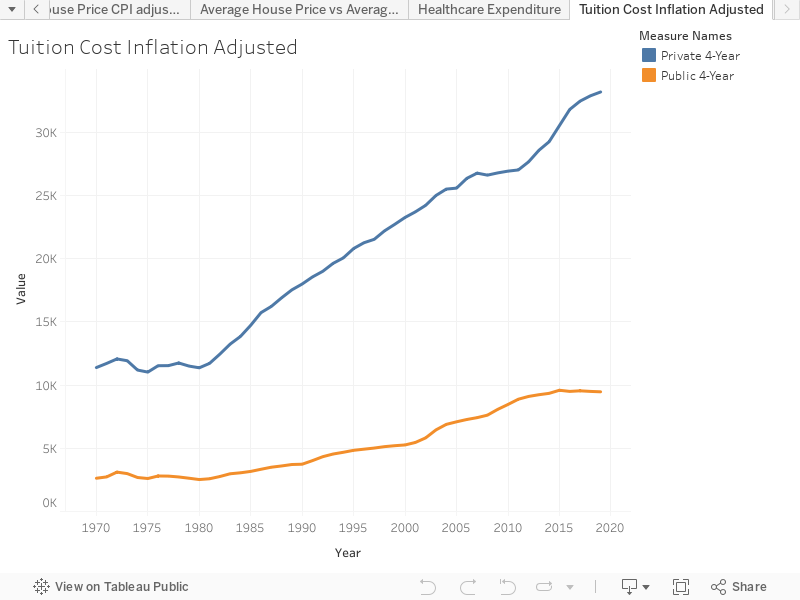

We can see that percentage of college graduates rose from 11.1% in 1970 to 37.5% in 2020. The more highly-educated professionals enter labor-force with significantly larger starting salaries, the higher the household income bracket should shift. The growth in the share of college graduates is constant except for the period between 2014 and 2020, where the growth was happening at a 1.7 times higher rate. At the same time, the share of households making $150,000 and over grew at a rate 2.1 times higher than average. Yet we must remember that correlation doesn't always mean causation, and a 1.7 times higher rate of graduates didn't directly cause a 2.1 times higher rate in household incomes. However, we can conclude that it was one of the key attributes that contributed to its growth. Therefore, a college degree is a crucial predictor of a high salary, but what about college costs? We will use National Center for Education Statistics data, adjust it for inflation, and plot the results:

As we can see, tuition has risen dramatically for both private and public schools. Since 1970, average tuition in private and public schools has increased by 2.9 and 3.6 times respectively. On the one hand, some of it can be explained by the ever-increasing entertainment, and sports value colleges have been adding in recent years and increased administrative expenses. On the other hand, in the case of private schools especially, like in any other part of the economy, higher demand results in a higher price.

To answer the question, why do 41% of people feel like life was better 50 years ago, we need to understand the fundamental shift in the economy. Over the last 50 years, most economic gains went to the educated upper-middle-class, while the middle and lower-income classes received none to little to gain. However, comparable income for the bottom 50 percentile does not do enough justice, as increased prices for healthcare and housing (driven by the US population) take a significantly larger share of paychecks. In addition, the cost of entering the upper-middle-class, aka higher education, is substantially more expensive. On top of that, something that we didn't discuss, now people have a novel spending category that people didn't have in 1970. It ranges from smartphones with its service and computers (that must be repurchased within 3-6 years) to streaming services and internet service. Thus with higher expenses bottom 50 percentile has less money available to spend on other life joys. 50 years ago, the economy was working best for workers majority, most of whom only had a high-school degree. In contrast, nowadays, the economy works best for the professional and educated minority. Although not in such a distant future, it won't be a minority anymore.

Philosophical note

I am not in the right to say what is fair and what is not. However, people who obtain higher education make a significant monetary and time-vise investment. As with most investments, they can pay off, and in some situations, they can be classified as a loss. But even if we diverge from investment idea, we can all admit that the world is changing, most production is getting automated, and there is no way back. The difference in income between highly educated individuals and those with a high-school degree will only expand further. I don't think the solution here is to leave things as-is, nor is it to implement extremely high taxes on high-earning individuals. I believe the solution is in the symbiosis of those two ideas as well as in making education more affordable for all.